Photo by Steve Johnson on Unsplash

NVIDIA Corporation (NVDA – Free Report) and Advanced Micro Devices, Inc. (AMD – Free Report) are at the center of the artificial intelligence (AI) hardware boom. Both companies make the graphics processing units (GPUs) and AI accelerators that train large language models, power cloud servers and drive modern computing.

However, as U.S. tariffs and new export restrictions weigh on tech sentiment, both stocks are down sharply this year. Year to date, NVDA and AMD stocks have plunged 22.2% and 27%, respectively.

YTD Stock Price Return Performance

Image Source: Zacks Investment Research

So, the question arises: Which chipmaker — NVDA or AMD — looks like the better AI play for investors amid the challenging macroeconomic backdrop? Let’s find out.

NVIDIA: The Dominant AI Force

NVIDIA is an undisputed leader in AI chips, data centers, gaming and autonomous vehicles. Its products are at the center of the ongoing AI revolution, driving demand from hyperscalers, enterprises and cutting-edge startups alike. The data center end-market continues to be a powerhouse for NVIDIA. Revenues from this end-market surged 93% year over year to $35.58 billion in the fourth quarter of fiscal 2025.

NVIDIA’s latest earnings call underscored the company’s continued AI dominance. CEO Jensen Huang highlighted the increasing demand for next-generation AI models that require unprecedented computational power. The company’s Blackwell architecture, capable of delivering up to 25 times the token throughput of its predecessor, is expected to drive the next wave of AI adoption.

Further bolstering its leadership, NVIDIA is set to launch its Blackwell Ultra and Vera Rubin platforms, which could solidify its position as the go-to AI infrastructure provider. With governments, corporations and cloud providers ramping up AI investments, NVIDIA remains the key beneficiary of this seismic shift in computing.

However, the recent restrictions imposed by the Trump administration on exporting H20 chips to China are likely to hurt NVIDIA’s overall financial growth in the near term. This has created a potential stumbling block. The company recently warned that export restrictions on China-customized H20 chips could cost it $5.5 billion in charges in the first quarter of fiscal 2026.

AMD: A Challenger With a Strong Portfolio

Advanced Micro Devices has steadily grown from an underdog into a formidable rival in high-performance computing. AMD is gaining traction in the cloud data center and AI chip markets with its portfolio of fifth-gen EPYC Turin, fourth-gen and third-gen EPYC processors, as well as Instinct accelerators and ROCm software suite.

Its MI300 series chips, designed to challenge NVIDIA’s dominance in AI, have received increasing attention from data center customers, with management signaling strong traction in early deployments. Data Center end-market revenues surged 69% year over year to $3.86 billion in the fourth quarter of 2024.

Advanced Micro Devices’ sustained focus on expanding its product portfolio will further bolster the company’s position in the AI chip space. AMD’s MI325X is currently under production. Its next-generation MI350 series, based on CDNA 4 architecture, promises a 35 times increase in AI compute performance compared with CDNA 3. The company plans to ship samples to lead customers in the current quarter and is on track to accelerate production shipments to mid-year.

The development of the MI400 series is also progressing well, and it remains on track to launch in 2026. To strengthen its AI ecosystem, Advanced Micro Devices has acquired several businesses, including ZT Systems, Helsinki-based Silo AI, Nod.ai and Mipsology.

Nonetheless, like NVIDIA, Advanced Micro Devices is also caught in the U.S.-China trade war crossfire. The Trump administration recently restricted exporting AMD’s MI308 to China, which the company believes will cost it approximately $800 million in charges related to inventory, purchase commitments and reserves.

Financials and Growth Outlook: NVIDIA Ahead by a Wide Margin

Though both companies have demonstrated strong financial performances in recent quarters, NVIDIA’s growth rate has exceeded Advanced Micro Devices’ by far. In the fourth quarter of fiscal 2025, NVIDIA’s revenues surged 78% year over year, while non-GAAP EPS climbed 71%. On the contrary, Advanced Micro Devices’ fourth-quarter 2024 revenues and non-GAAP EPS soared 24% and 31%, respectively.

Analysts’ projections for the current and next fiscal year suggest higher growth potential for NVIDIA. The Zacks Consensus Estimate for NVIDIA’s fiscal 2026 and 2027 revenue projects year-over-year growth of 52% and 23%, respectively. Non-GAAP EPS is expected to rise 47% in fiscal 2026 and 24% in fiscal 2027.

NVIDIA Corporation Stock Price, Consensus and EPS Surprise

NVIDIA Corporation price-consensus-eps-surprise-chart | NVIDIA Corporation Quote

On the contrary, the consensus mark for Advanced Micro Devices’ 2025 and 2026 revenues indicates a year-over-year increase of 23% and 19%, respectively. Non-GAAP EPS is projected to rise 39% in 2025 and 31% in 2026.

Advanced Micro Devices, Inc. Stock Price, Consensus and EPS Surprise

Advanced Micro Devices, Inc. price-consensus-eps-surprise-chart | Advanced Micro Devices, Inc. Quote

Additionally, NVDA has been witnessing positive earnings estimate revisions. The Zacks Consensus Estimate for NVIDIA’s fiscal 2026 earnings is pegged at $4.41 per share, up 2 cents over the past 30 days. On the contrary, analysts have lowered their 2025 earnings estimates for AMD to $4.59 per share from $4.60 expected seven days ago.

Valuation: Higher Growth Trajectory Justifies NVDA’s Premium

Valuation-wise, both NVIDIA and Advanced Micro Devices are overvalued, as suggested by the Zacks Value Score of D.

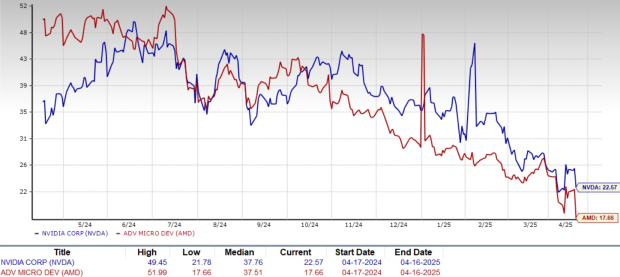

However, in terms of forward 12-month Price/Earnings, AMD shares are trading at 17.66X, lower than NVDA’s 22.57X.

Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

While NVIDIA commands a premium over Advanced Micro Devices, its valuation is justified, given its superior growth trajectory. Though both companies play crucial roles in the semiconductor industry, investors should recognize that NVIDIA’s premium valuation is backed by its unparalleled dominance in the fastest-growing AI and high-performance computing areas.

Final Thoughts: NVDA is the Smarter Buy Right Now

Both NVIDIA and Advanced Micro Devices are deeply embedded in the AI revolution, with compelling growth narratives and product roadmaps. However, NVIDIA’s dominant market position with groundbreaking technology, robust financials and an expanding market presence makes it a better investment choice. Though NVDA stock might seem pricey against AMD, its premium valuation is justifiable considering the higher growth expectations.

Currently, NVDA has a Zacks Rank #2 (Buy), making the stock a must-pick compared with AMD, which has a Zacks Rank #3 (Hold).

More By This Author:

Alphabet Earnings Expected To Grow: What To Know Ahead Of Next Week’s Release

Buy These Defensive Stocks After Beating Earnings Expectations?: ACI, JNJ

Earnings Preview: AT&T Q1 Earnings Expected To Decline