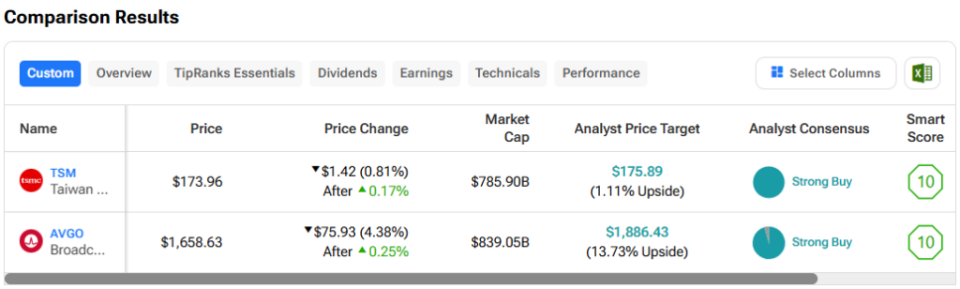

In this piece, I evaluated two semiconductor stocks, Taiwan Semiconductor Manufacturing (NYSE:TSM) and Broadcom (NASDAQ:AVGO), using TipRanks’ Comparison Tool to see which is the better buy. A closer look suggests a bullish view of TSM and a neutral view of Broadcom.

Taiwan Semiconductor Manufacturing manufactures and sells semiconductors for several end markets, including gaming consoles, servers, tablets, and computers, the automotive market, the Internet of Things, and other digital consumer electronics. On the other hand, Broadcom’s chips target the renewable energy, automotive, military and aerospace, industrial, and robotics markets.

Shares of TSM have soared 71% year-to-date and are up 76% over the last year. Meanwhile, Broadcom stock has jumped 49% year-to-date and is up over 100% in the last year.

The differing 12-month returns of TSM and Broadcom are suggestive of the concerns some Americans may have with holding Taiwanese stocks.

China has long seen Taiwan as part of its territory — even though Taiwan rules itself. As a result, China has been increasing its threats against and military exercises around the small island. Of course, uncertainties like that are enough to make many investors nervous, but there’s more to the story when comparing TSM and Broadcom.

We’ll compare their price-to-earnings (P/E) ratios to gauge their valuations against each other and that of their industry. For comparison, the semiconductor industry is trading at a P/E of 68.8x versus its three-year average of 34.6x.

Taiwan Semiconductor Manufacturing (NYSE:TSM)

At a P/E of 34.4x, Taiwan Semiconductor Manufacturing is trading at a steep discount to Broadcom and many other U.S. semiconductor names. Plus, without TSM, some of the world’s best-known semiconductor names wouldn’t have any products. Thus, a bullish view seems appropriate.

The biggest difference between TSM and Broadcom is that TSM operates as a foundry, meaning it manufactures chips for other companies like Intel (NASDAQ:INTC). In fact, TSM is the world’s largest contract chipmaker, and it’s the one that actually manufactures those artificial-intelligence chips that have driven Nvidia’s (NASDAQ:NVDA) stock price higher and higher in recent years.

On Tuesday, TSM shares popped after DigiTimes reported that Intel had chosen the company to manufacture its new 3-nanometer chips for its new notebook computers. DigiTimes had reported in May that TSM was already at a 95% utilization rate for its 3-nanometer production, so adding Intel’s chips may well bring the company to full utilization or close to it.

Given how high TSM’s utilization rates are running and how cash-rich its customers are, it’s clear that the company has the pricing power to raise prices, so we can expect revenue growth to remain strong. The company is also building three new fabrication facilities in Arizona so that it can support even more customers while tapping into U.S. incentives for domestic semiconductor manufacturing.

Some investors may still be concerned about the fact that TSM is a Taiwanese company. However, it’s worth noting that TSM’s U.S.-listed American depository receipt (ADR) shares are trading at more than a 20% premium to the company’s Taiwan-listed stock — the widest gap in over 10 years.

As that gap grows wider, it suggests investors may be becoming less concerned about those long-running geopolitical concerns. Additionally, as TSM moves some of its manufacturing outside Taiwan, the potential risks associated with investing in the company fall.

Therefore, this could be a good time to buy this deeply discounted stock before it starts to approach valuations in line of major U.S. chipmakers like Broadcom and Nvidia.

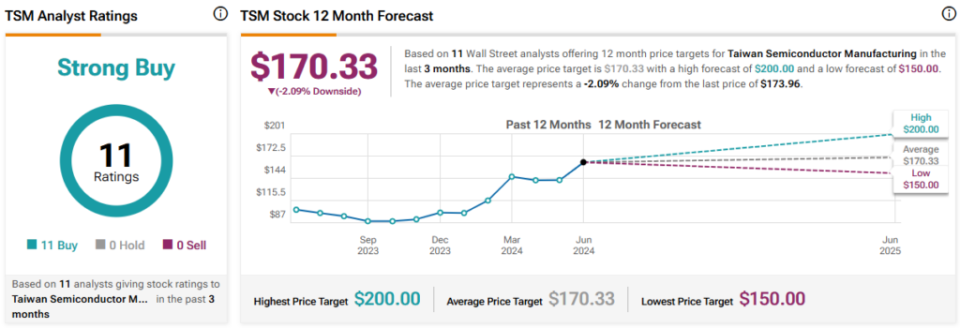

What Is the Price Target for TSM Stock?

Taiwan Semiconductor Manufacturing has a Strong Buy consensus rating based on 11 Buys, zero Holds, and zero Sell ratings assigned over the last three months. At $170.33, the average TSM stock price target implies downside potential of 2.1%.

Broadcom (NASDAQ:AVGO)

At a P/E of 74.6x, Broadcom is trading at a premium to its industry but in line with top AI chipmakers like Nvidia, which is at a P/E of 76.5x. At the current valuation, Broadcom is trading roughly in line with its last two peaks in December 2020 and February 2021, when it was trading at a P/E just below 80x. Thus, a neutral view seems appropriate — pending a more attractive entry price.

Broadcom is largely a fabless semiconductor company, meaning it outsources its chip manufacturing to foundry operators like TSM. In fact, TSM manufactured 90% of Broadcom’s semiconductors as recently as 2022, although Broadcom does operate three small fabs that represent a minuscule part of its business, according to its 2022 annual filing.

Broadcom shares received a significant bump following the latest earnings report on June 12, which was accompanied by an announcement about a 10-for-one stock split. AVGO stock has pulled back since then, falling roughly $100. However, a steeper drop seems likely eventually, especially considering that its Relative Strength Index was over 70 this week (although it finally came down today), which suggests overbought territory. The downside is that we might have to wait a while to see a better price.

Broadcom will conduct its 10-for-one stock split on July 12, and the shares will start trading at their split-adjusted price on July 15. For investors looking for bargains, the problem with stock splits like this one is that they tend to temporarily inflate a company’s share price as more investors pile into the stock.

A stock split doesn’t actually change the company’s value. It just makes the shares more accessible to retail investors who don’t have a massive portfolio and won’t or can’t really afford to pay $1,660 for a single share. At $166 per share, Broadcom stock seems much more reasonably priced, but the overall valuation is the same because there are 10 times more shares when the price is cut to one-tenth of the current price.

Once we get past the stock split and its associated noise, it seems likely that a more attractive entry price will come around.

What Is the Price Target for AVGO Stock?

Broadcom has a Strong Buy consensus rating based on 21 Buys, two Holds, and zero Sell ratings assigned over the last three months. At $1,886.43, the average Broadcom stock price target implies upside potential of 13.7%.

Conclusion: Bullish on TSM, Neutral on AVGO

Taiwan Semiconductor Manufacturing and Broadcom are both excellent semiconductor companies with long-term track records of success and bright futures. However, TSM isn’t getting its share of the glory for being the company that manufactures so many of the chips that have made Broadcom and many others into AI darlings.

At some point, TSM could earn a P/E multiple in line with Broadcom, Nvidia, and others, so this seems like a great time to buy. On the other hand, Broadcom’s valuation already looks full, so patience is needed for a better entry price.

")